Introduction

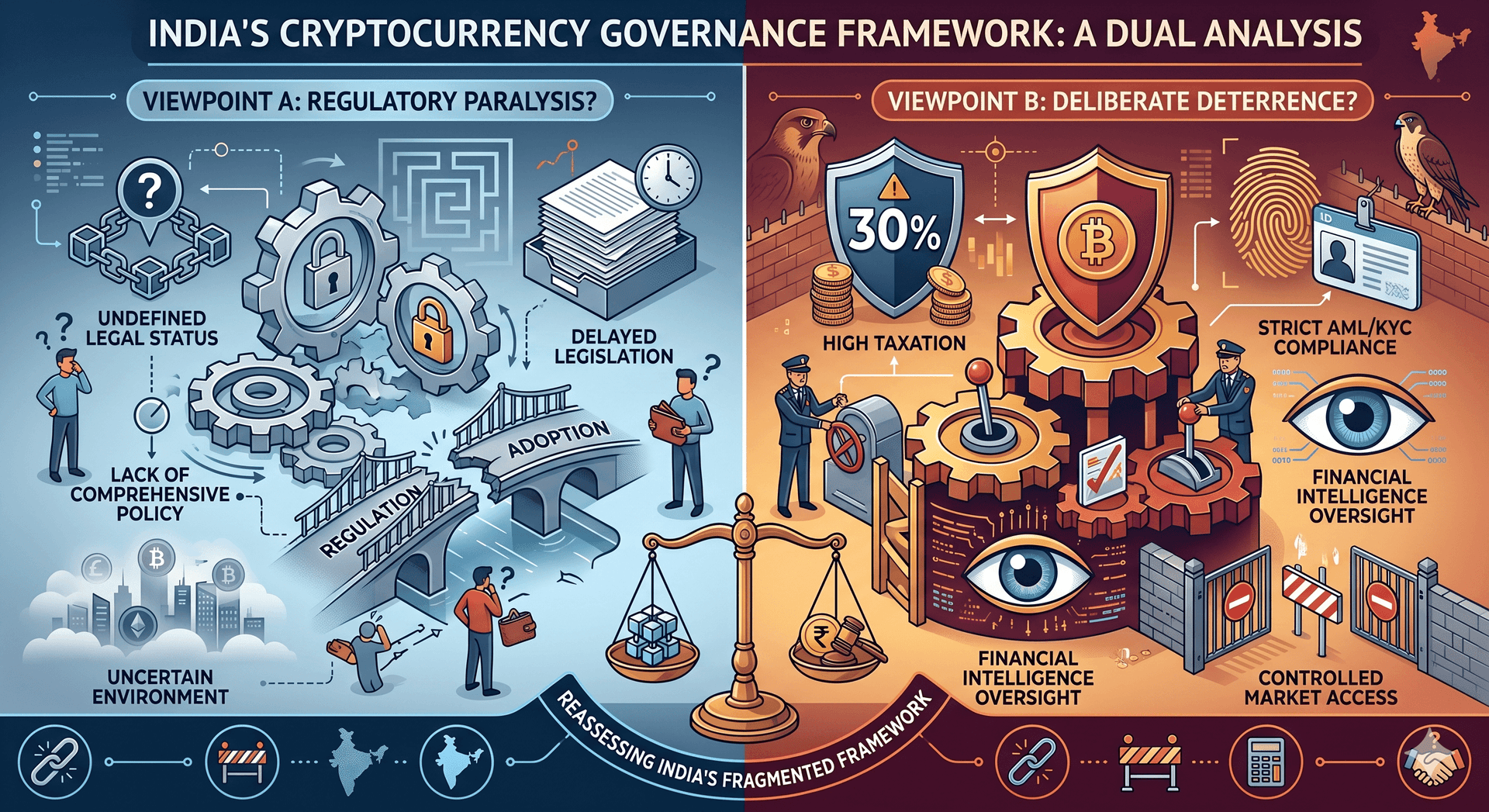

The Indian government applies multiple compliance requirements to cryptocurrencies which remain undefined according to official regulations. The current regulatory framework functions through three main elements which include judicial decisions, anti-money laundering guidelines, and tax penalties that respond to distinct policy requirements without following any established legal framework. The article demonstrates that India's control over virtual digital assets works through deterrent mechanisms which produce market disruptions and create unfair advantages for international companies while hindering India's ability to compete in worldwide digital asset transactions. The research study investigates whether the absence of basic legal requirements for compliance duties which have been imposed by authorities creates actual regulatory requirements or just invents them.

India operates one of the largest retail cryptocurrency user bases worldwide while maintaining a skilled technology workforce and a payment system that has achieved worldwide interoperability. The existing structural benefits of the organization have failed to establish its position as a leader in regulatory matters. The existing governance void has been gradually established through three main methods which include court decisions, government announcements, and tax regulations while the European Union and Singapore have developed complete legal systems which have brought institutional investments and research facilities to their regions that India has successfully exported. The situation exists because of intentional government strategies which aim to restrict cryptocurrency activities instead of implementing official rules.

Regulatory Ambiguity and the Architecture of Control

The Supreme Court decision in Internet and Mobile Association of India v Reserve Bank of India created a constitutional turning point for India when it declared the Reserve Bank of India 2018 circular which ordered financial institutions to stop working with cryptocurrency businesses as unconstitutional because it imposed excessive restrictions. The Court found that the RBI had demonstrated anticipated risk rather than proven harm. The legislative process should have been initiated by this court decision. The Lok Sabha bulletin contained the Cryptocurrency and Regulation of Official Digital Currency Bill 2021 yet Parliament did not take any action to bring it forward. The authorities decided to govern through a legislative vacuum which they created because the resulting expenses from this decision have now become evident to everyone.

The RBI has maintained an antagonistic relationship with its institutional opponents. The organization maintains control over payment systems and banking services to cryptocurrency businesses through methods which escape formal legal assessment thus creating a situation where the organization can control operations without being bound by official rules. When an organization uses unofficial methods to control its operations, all affected parties lose their right to understand which legal standards apply and their ability to challenge decisions which negatively impact them. This system enables the organization to maintain power while avoiding all responsibility to regulatory standards. The comparative deficit contains a significant structural deficit. The EU's Markets in Crypto-Assets Regulation MiCA which becomes fully operational in December 2024 establishes a legal framework that defines crypto-assets and permits licensed operators to provide services throughout Member States. The Payment Services Act of 2019 Singapore allows digital payment token services to operate under three different compliance tiers which match their risk assessment needs. Both systems have successfully attracted institutional capital together with infrastructure needed for Web3 development. India, through its regulatory approach, has created opposite results. Regulation that drives regulated conduct beyond the regulator's jurisdiction does not mitigate risk it relocates risk beyond the regulator's reach.

Compliance Without Clarity Taxation, PMLA, and Market Distortion

India's March 2023 notice which extended the Prevention of Money Laundering Act 2002 to virtual digital asset service providers, who must now obtain FIU-India registration and conduct customer due diligence and report suspicious transactions, achieved only minimal compliance with FATF Recommendations about Virtual Assets. The alignment is formal rather than substantive. PMLA compliance on an unclassified asset category results in permanent interpretative uncertainty whereas anti-money laundering regulations for virtual digital assets fail to determine asset ownership and contractual enforcement rights and the status of decentralized systems which operate without a central governing entity. The absence of defined compliance requirements acts as a barrier which prevents smaller platforms from accessing markets while it enables larger organizations to create tax compliance frameworks and operational methods which handle unclear legal obligations. The Finance Act 2022 established a 30% flat tax on VDA transfer income which prohibits deduction of losses and prevents offsetting against other income categories and also imposes a 1% tax deduction at source under Section 194S of the Income Tax Act 1961. This framework is not revenue-optimised because it actively works to suppress operations through its built-in design. A 30% tax on total revenue from a fluctuating asset category operates as a transaction-based tax instead of an economic profit tax. The documented consequence migration of trading volumes from Indian exchanges to offshore platforms confirms the deterrent objective was achieved while contracting the taxable base. Retail users who follow regulations because they use unregulated offshore platforms face increased systemic risk, which creates an unsafe situation for users who lack domestic consumer protection safeguards. The compound effects create obstacles for banking access and generate disruptions in payment gateways and result in institutional financial institutions stopping their business dealings.

Reforms & Recommendations

The fundamental reform which India needs requires the creation of a Virtual Digital Assets Act which will establish three legislative functions that currently do not exist. First, a statutory taxonomy which separates payment tokens and utility tokens and security tokens and stablecoins will create definitions which resolve ambiguity in financial sectors and tax systems and investor protection areas. Second, a designated regulatory jurisdiction which establishes institutional boundaries between the RBI and SEBI and the FIU through a lead-regulator model designates SEBI as the main regulatory body for investment-instrument crypto-assets while the RBI maintains control over payment tokens and stablecoin issuers through inter-agency coordination which formalizes their relationship via the Financial Stability and Development Council. Third, a licensing framework will create enforceable rights and obligations which permit judicial review while the system will eliminate governance through informal administrative pressure.

Tax systems need to undergo fundamental changes which should focus on facilitating market growth instead of creating obstacles for market operators. The current 30% flat tax rate should be replaced with a capital gains tax system which establishes different rates based on how long assets are held. Loss carryforward within the VDA asset class must be permitted to reflect economic reality. The TDS rate under Section 194S should be recalibrated to a level sufficient for transaction monitoring between 0.01% and 0.1% without constituting a liquidity penalty. Higher revenue volumes will produce revenue neutrality according to the governing principle which demonstrates that a rationalized structure will generate more tax revenue through domestic participation than a prohibitive rate which will drive taxable entities out of the system.

Regulatory coordination needs to become a formalized process. The Inter-Regulatory Technical Group under the FSDC should extend its territory to include VDA governance by creating a unified classification system through its statutory power.

Conclusion

India lacks a cryptocurrency governance framework because its system comprises reactive measures which include a judicial decision that occurred without any legislative answer and an anti-money laundering regulation that lacks proper definitions and a tax framework which was designed to restrict activities instead of recording them and a system which maintains institutional barriers through unofficial methods that exist outside official legal procedures. The question of whether this constitutes regulatory strategy or regulatory paralysis resolves, on evidence, in favour of the latter. The jurisdiction has expanded its compliance requirements without passing any new laws so it has chosen to postpone its policy decision which now creates negative impacts on its markets and tax revenue and global standing. The proposed reforms need political commitment to solve the power struggle between institutions and they need financial discipline to allow temporary revenue changes which will support long-term market growth and they need lawmakers to recognize virtual digital assets as a governance issue which requires legal solutions instead of treaties. India has the necessary institutional power and technological capabilities and large population to become a major governance center for worldwide digital asset regulation. The political economic forces which support regulatory delay will determine whether the need for strategic legal development will prevail. The expenses associated with ongoing postponement have reached a non-speculative stage because they have been completely documented and they show a definite upward trend.